Stop losing deals to

spreadsheets.

Eight AI tools in one command center. From motivated seller to signed LOI — faster than your competition can open Excel.

8 Tools. One Platform.

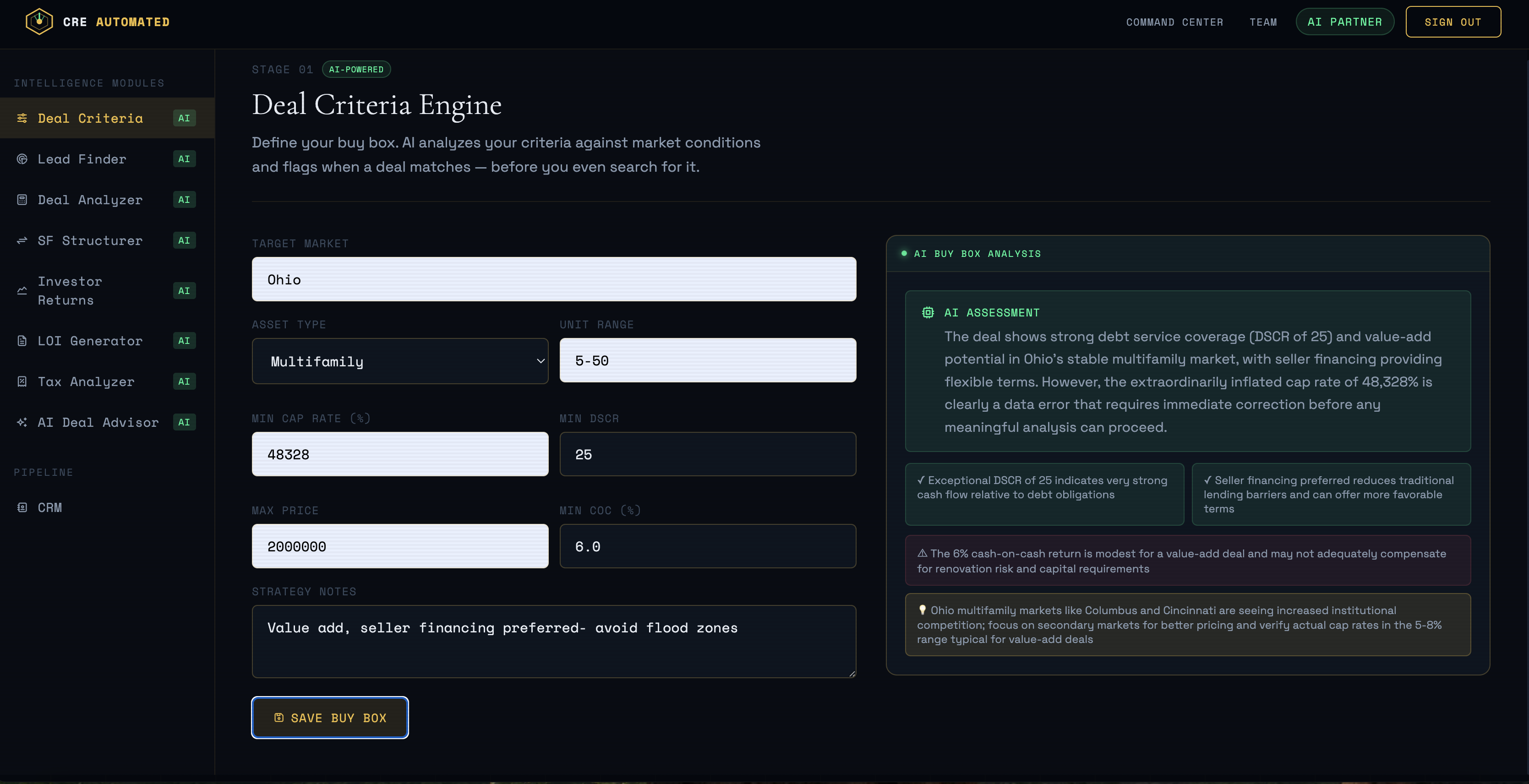

Every stage of the CRE deal — from first look at a lead to the signed LOI — lives in one command center. No spreadsheets. No switching apps. No copy-pasting between tools.

Access all 8 tools →

Motivated seller to signed LOI

in under 5 minutes.

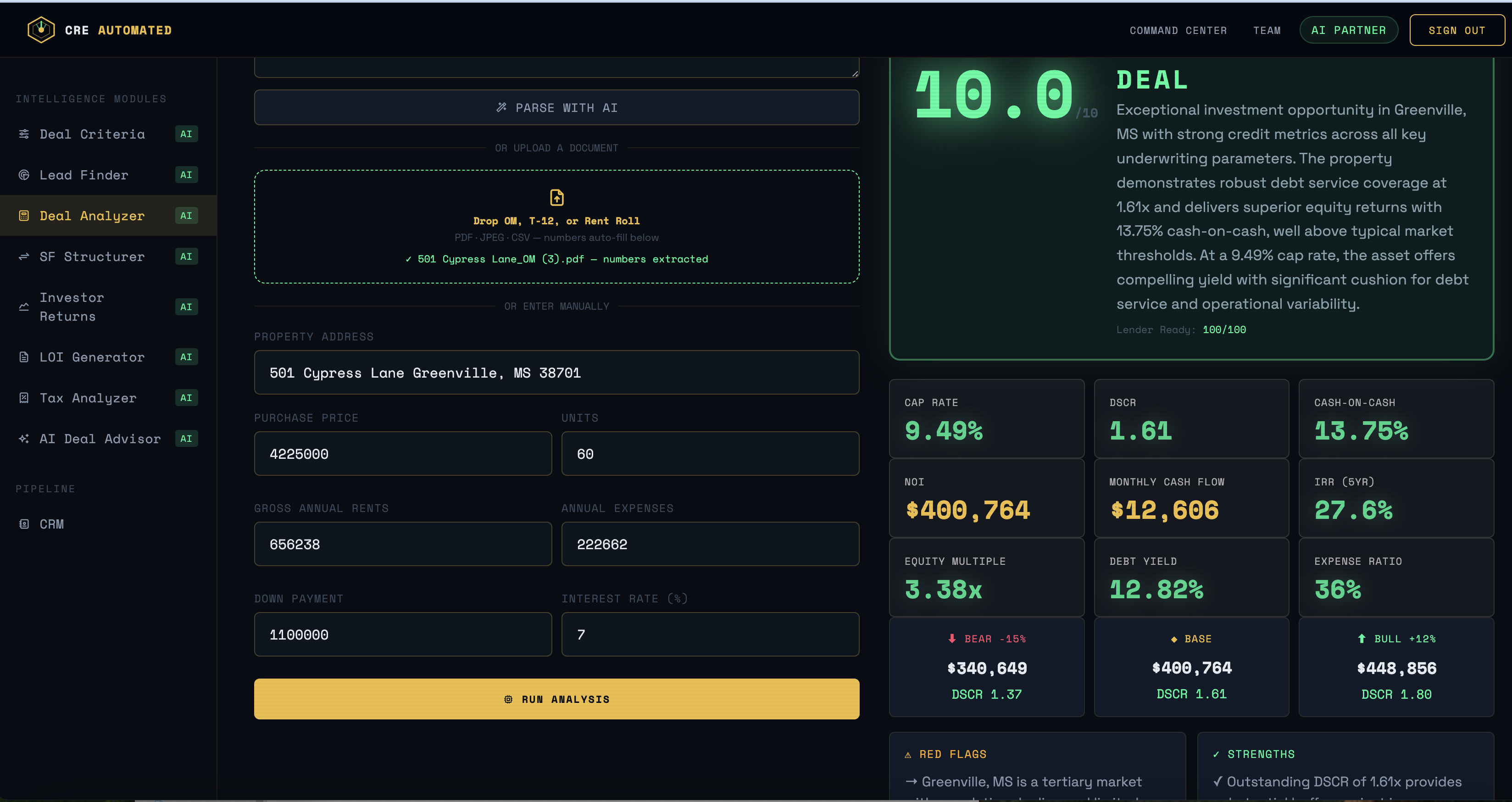

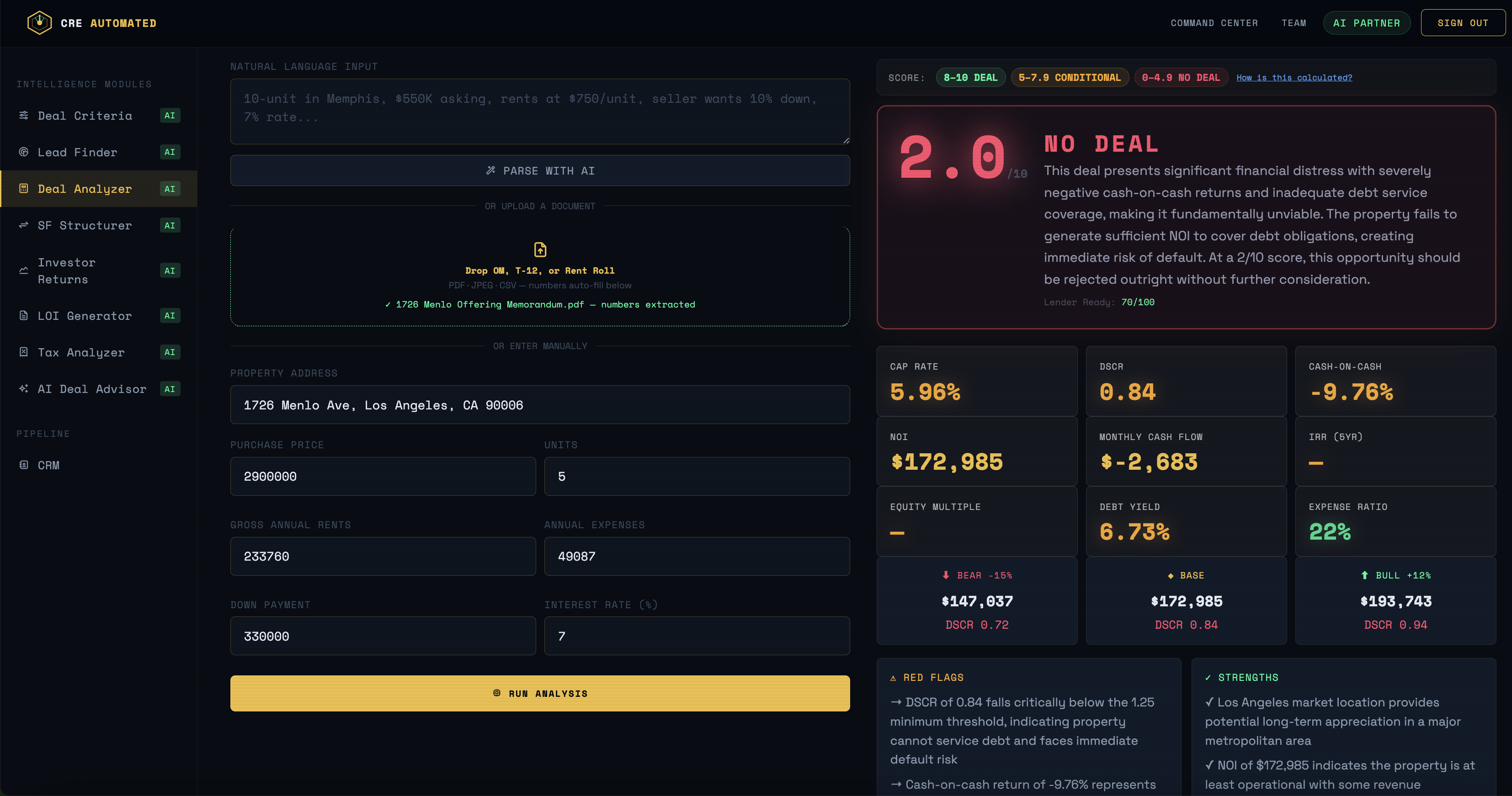

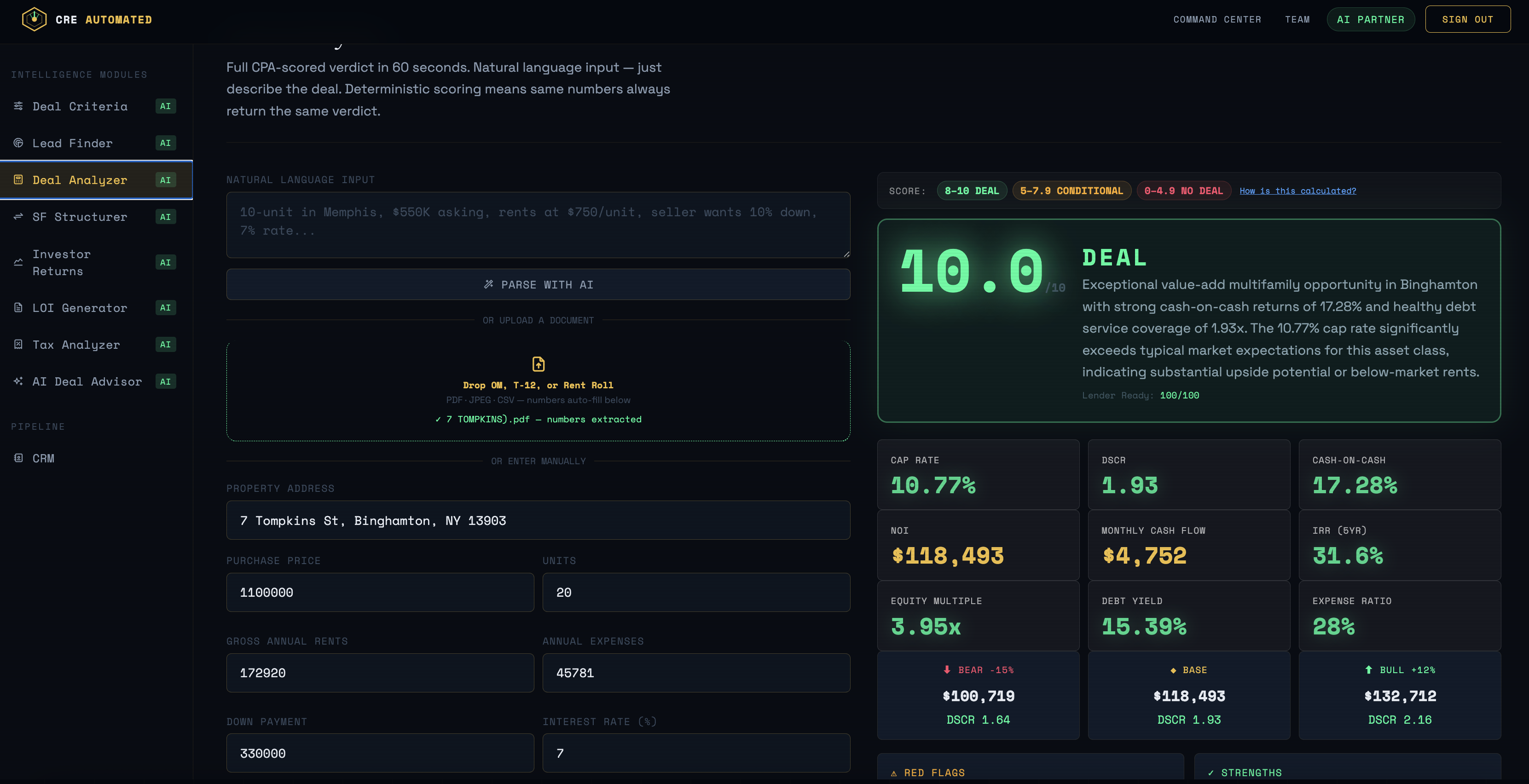

The average investor spends 4 hours underwriting one deal. Here's what happens when AI does it.

"I built the tool I needed myself — because nothing else went past the lead list."

I've been investing in commercial real estate in Louisiana and Mississippi for years. Every time I found a motivated seller, I'd spend hours in Excel trying to figure out if the deal actually worked. Then I'd write an LOI from scratch. Then model the returns for my investors. Then figure out the tax implications.

None of the "CRE tools" on the market helped with any of that. PropStream finds the lead. Then you're on your own.

So I built CRE Automated — one command center that takes you from motivated seller CSV all the way to a signed LOI, with every number calculated and every document generated by AI. I use it on every deal I look at. Now you can too.

Real screens.

Real deals.

This is what the command center looks like on live deals — not demo data, not stock photos.

Cancel PropStream.

We already have the leads.

PropStream, PropertyRadar, ParGo give you a list and stop. CRE Automated has 160M+ properties built in — plus AI that finds motivated sellers automatically — and does everything after the lead too.

Deals closed.

Spreadsheets cancelled.

"I uploaded an OM and had a full underwriting report in under 60 seconds. I'd been spending 3 hours per deal in Excel. This is what I was looking for."

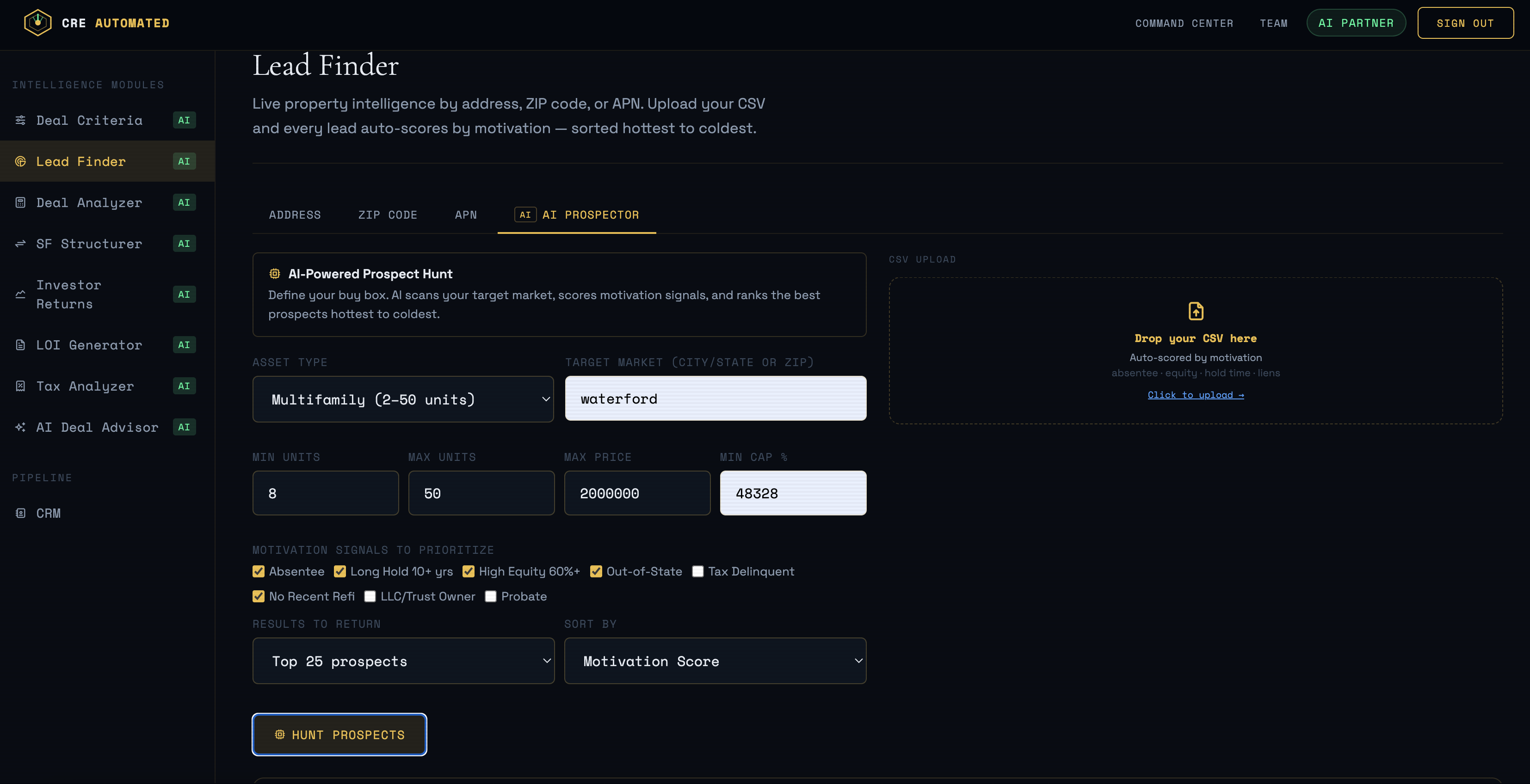

"The CSV upload and auto-scoring changed everything. I was manually rating leads. Now the hottest deals surface themselves. Made an offer on a 9/10 the same day I found it."

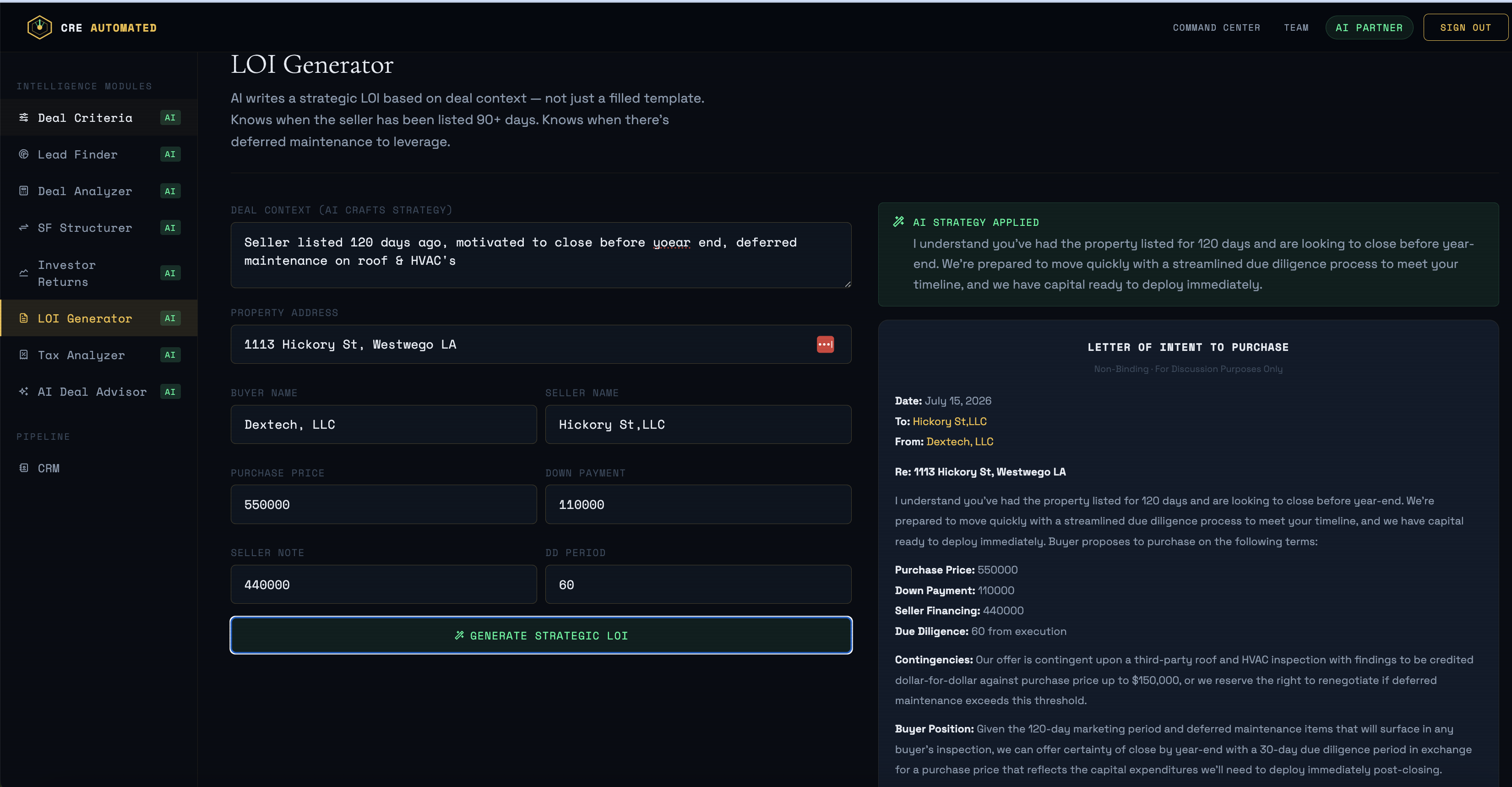

"The seller financing pitch generator is worth the subscription alone. It told me to lead with the installment sale tax angle. The seller was already thinking about taxes. Worked perfectly."

Simple pricing.

No per-seat surprises.

AI Partner includes unlimited team seats at no extra charge. Everyone gets the same AI — Analyst is single-user, Elite is up to 5, Partner is your whole team.

- Deal Analyzer — 60s CPA scoring

- Buy box match on every analysis

- Lead Finder — ATTOM · ZIP · APN

- Upload CSV + motivation scoring

- SF Structurer + LOI Generator

- CRM Pipeline + AI Daily Brief

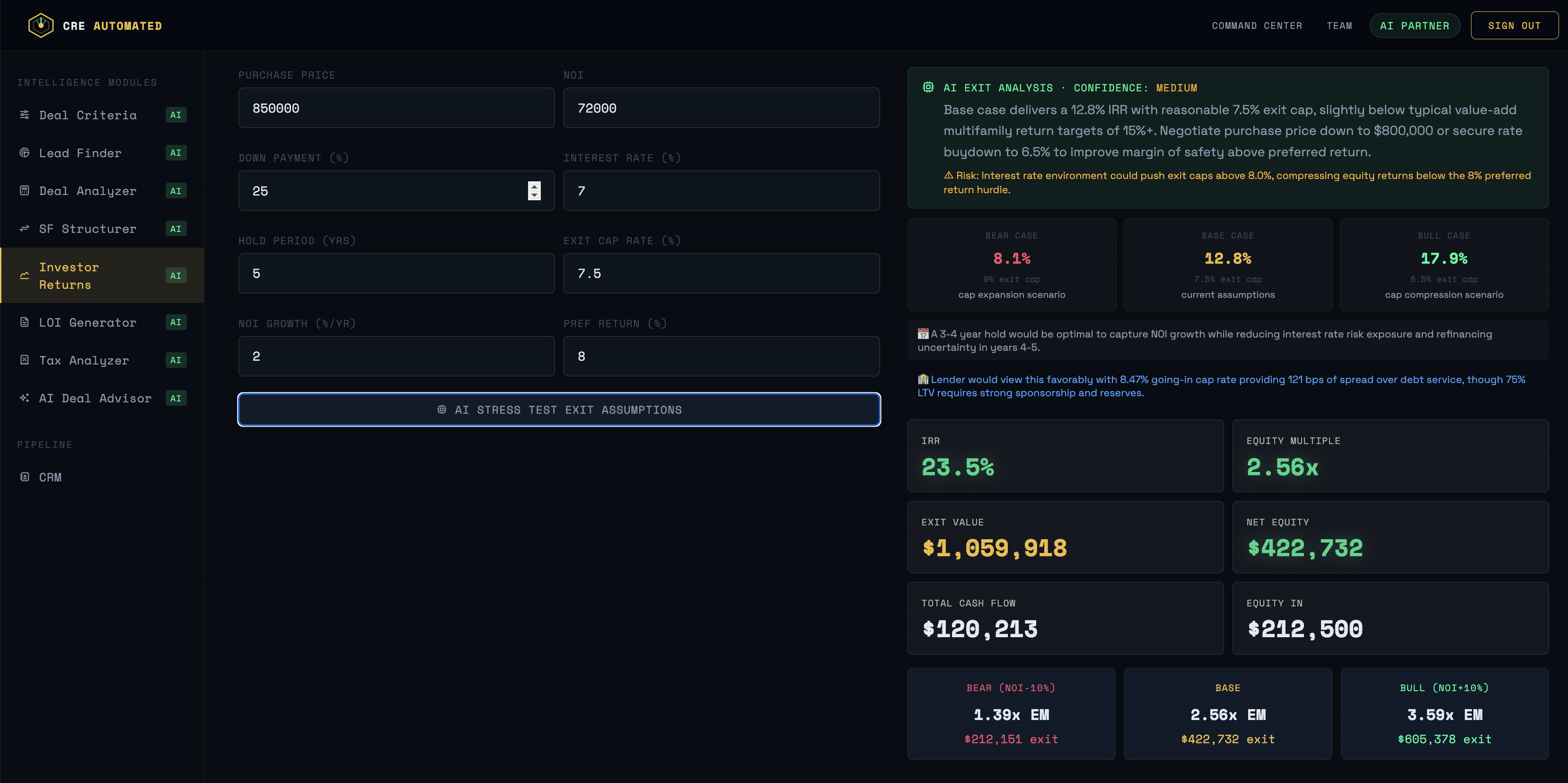

- Investor Returns + Stress Tests

- AI Deal Advisor (OM upload)

- Everything in Analyst

- Investor Returns — IRR · equity multiple

- Exit Cap Sensitivity + 5-Year Hold Projection

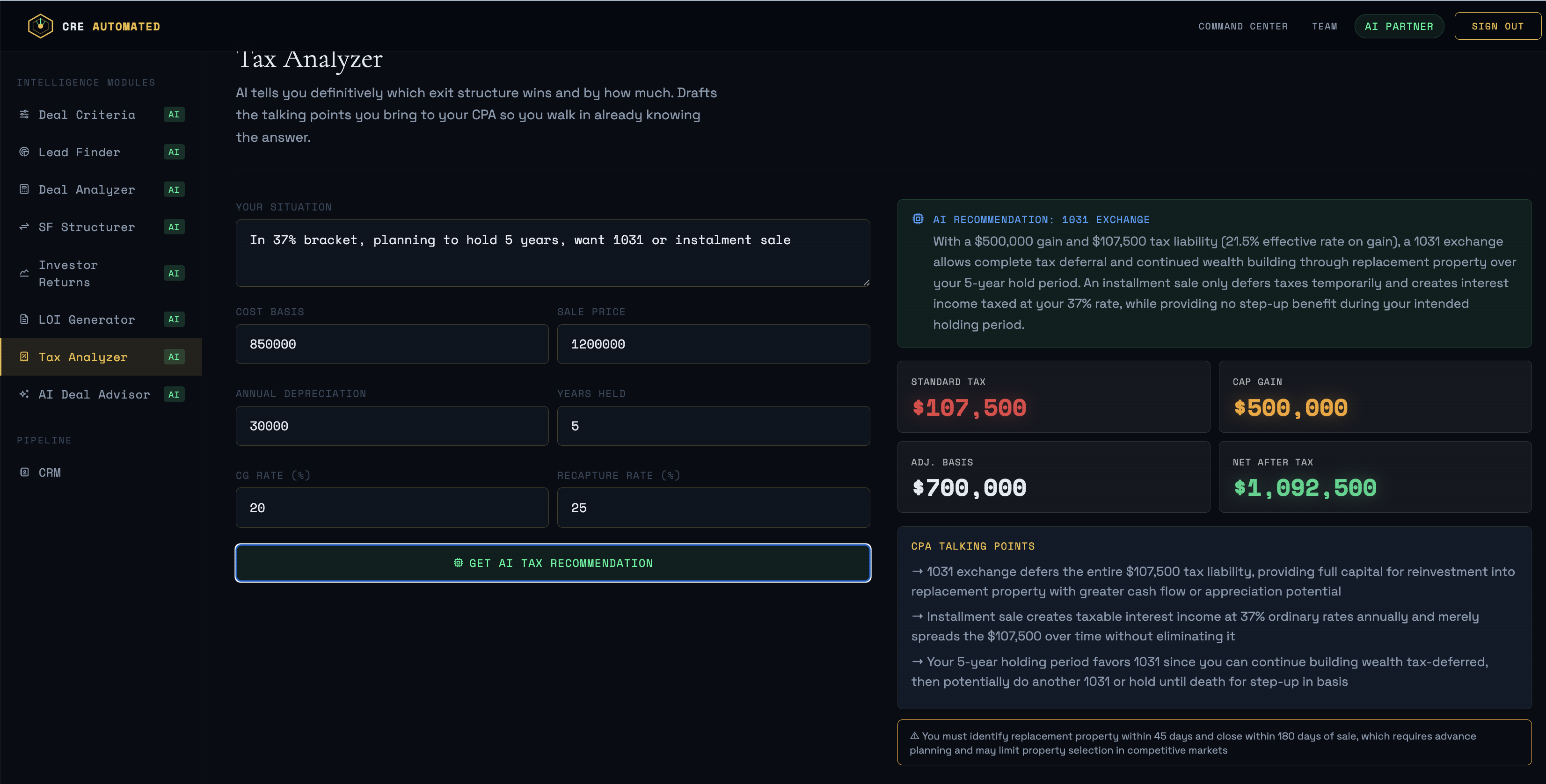

- Tax Analyzer — 1031 · installment · DST

- AI seller pitch + LOI tone revision

- Natural language OM parsing

- AI Deal Advisor — upload any OM

- Skip trace + AI Prospector

- Full Institutional Deal Package (PDF)

- Unlimited team seats

- Everything in Elite

- Unlimited team seats — no per-user charge

- Daily motivated seller alerts by market

- AI monitors your markets 24/7

- Shared CRM — full team pipeline visibility

- Buy box learns from every team close

- LOI review + CPA talking points

Common questions,

straight answers.

The deal is gone before

your spreadsheet loads.

Pick a plan and get instant access to all 8 AI tools. Or try 1 free analysis first on DealVerdict — then come back ready to subscribe.

DealVerdict — 1 free CPA-scored deal analysis. No card required.